Truth in Lending

Understanding Personal Loans Online Lenders

Effective Date: 2026

At SmallPersonalLoansOnline.com, we believe consumers deserve clear, transparent information regarding borrowing costs, repayment obligations, and loan terms before making financial decisions. This Truth in Lending page is designed to help visitors understand important lending concepts and the disclosures that lenders may provide during the application and approval process.

Federal lending laws are intended to promote transparency and help consumers compare financial products more effectively. Understanding these disclosures can help borrowers make informed decisions and avoid unexpected costs.

This page explains common lending disclosures, borrowing terminology, repayment obligations, and consumer rights.

What Is Truth in Lending?

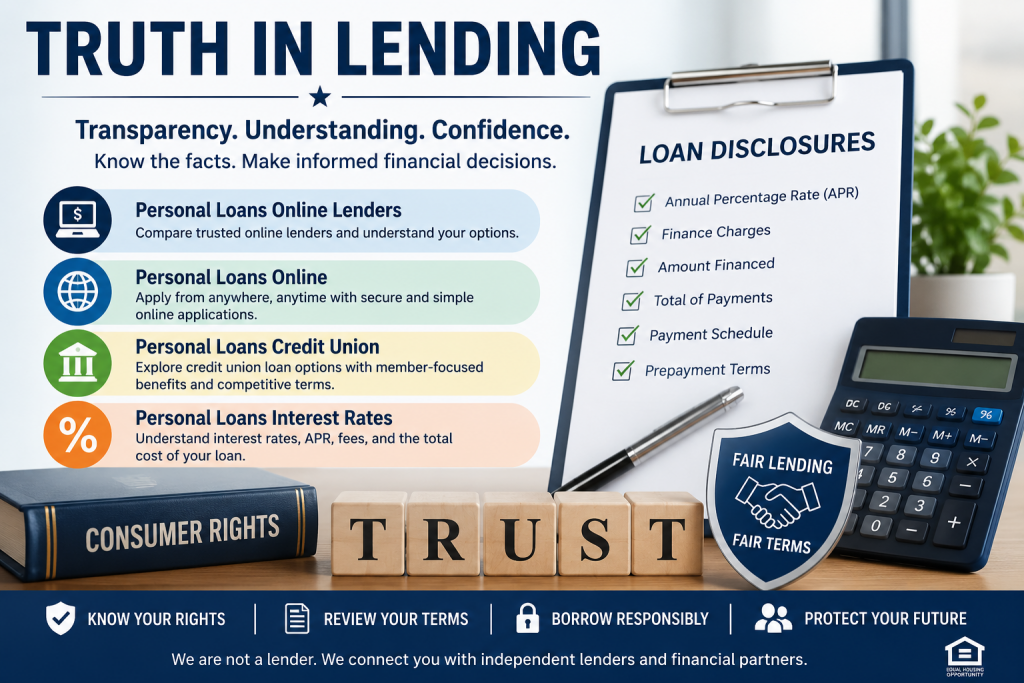

Truth in Lending refers to federal disclosure requirements designed to help consumers understand the cost of borrowing.

These requirements generally encourage transparency regarding:

- Annual Percentage Rate (APR)

- Finance charges

- Repayment schedules

- Total loan costs

- Payment obligations

- Fees and charges

The goal is to help borrowers compare lending products more effectively before accepting financing.

Understanding Personal Loans Online Lenders

Many consumers research Personal Loans Online Lenders because online lending platforms often provide convenient access to loan information and application tools.

Educational resources discussing Personal Loans Online Lenders help consumers understand how digital lending works and what information lenders may disclose during the application process.

Why Lending Disclosures Matter

Borrowing money creates a legal obligation to repay the loan according to agreed terms.

Before accepting financing, consumers should carefully review:

- Interest rates

- Repayment terms

- Monthly payment amounts

- Loan fees

- Total borrowing costs

Understanding these details can help borrowers determine whether a financial product fits their needs and budget.

Important Lending Terms

Annual Percentage Rate (APR)

APR represents the cost of borrowing expressed as a yearly percentage.

APR may include:

- Interest charges

- Certain lender fees

- Financing costs

Consumers often use APR when comparing lending products because it provides a standardized measurement.

Finance Charges

Finance charges represent the total cost of obtaining credit.

These charges may include:

- Interest

- Origination fees

- Certain administrative costs

Total Payment Amount

The total payment amount reflects the full cost of the loan if all payments are made according to schedule.

Understanding Personal Loans Online

The internet has significantly changed the lending industry.

Consumers increasingly research Personal Loans Online because digital platforms often allow borrowers to compare options, review disclosures, and complete applications without visiting physical locations.

Many online lending platforms provide educational resources designed to help consumers understand borrowing obligations before accepting loan offers.

Benefits of Reviewing Disclosures

Reviewing loan disclosures may help consumers:

- Compare offers

- Understand repayment schedules

- Evaluate affordability

- Identify fees

- Calculate total borrowing costs

Informed borrowers are generally better positioned to make responsible financial decisions.

How Loan Payments Work

Most personal loans involve fixed monthly payments.

A payment may include:

- Principal repayment

- Interest charges

- Applicable fees

The exact structure varies depending on lender requirements and loan terms.

Repayment Periods

Common repayment periods may range from:

- Several months

- Multiple years

Longer repayment periods often reduce monthly payments but may increase total borrowing costs.

Shorter repayment periods may result in higher monthly payments while reducing overall interest expenses.

Understanding Personal Loans Credit Union

Many consumers compare lending options offered through banks and Personal Loans Credit Union programs.

Credit unions often operate as member-focused financial institutions and may offer various lending products depending on membership eligibility and qualification requirements.

Educational content regarding Personal Loans Credit Union options can help consumers better understand available borrowing alternatives.

Borrower Responsibilities

Consumers should carefully review all loan documents before signing.

Borrowers are generally responsible for:

- Making payments on time

- Understanding loan terms

- Reviewing disclosures

- Monitoring account activity

- Communicating with lenders regarding payment issues

Failure to meet repayment obligations may have financial consequences.

Potential Consequences of Missed Payments

Missed payments may result in:

- Additional fees

- Collection activity

- Credit reporting impacts

- Increased financial obligations

Borrowers should contact lenders promptly if financial difficulties arise.

Understanding Loan Fees

Some lending products may involve fees.

Examples include:

- Origination fees

- Late fees

- Returned payment fees

- Administrative fees

Consumers should review disclosures carefully to identify all potential costs.

Evaluating Total Cost

Interest rates alone do not always reflect total borrowing costs.

Consumers should review:

- APR

- Fees

- Repayment term

- Total payment amount

These factors collectively influence affordability.

Understanding Personal Loans Interest Rates

One of the most important borrowing considerations involves Personal Loans Interest Rates.

Interest rates influence:

- Monthly payment amounts

- Total borrowing costs

- Overall affordability

Educational resources discussing Personal Loans Interest Rates help consumers understand how borrowing costs are calculated and compared.

Factors That May Influence Rates

Lenders may consider various factors, including:

- Credit history

- Income

- Debt obligations

- Employment information

- Loan amount

- Repayment term

Qualification requirements vary among lenders.

Consumer Rights

Federal and state laws provide various consumer protections.

These protections may include:

- Disclosure requirements

- Fair lending standards

- Complaint procedures

- Privacy protections

Consumers should familiarize themselves with applicable rights before entering financial agreements.

Comparing Loan Offers

Consumers are encouraged to compare multiple offers whenever possible.

Important comparison factors include:

- APR

- Monthly payment

- Repayment term

- Fees

- Total repayment amount

Careful comparison may help consumers identify options that align with their financial goals.

Additional Information About Personal Loans Online Lenders

Consumers researching Personal Loans Online Lenders should carefully review lender disclosures, qualification requirements, and repayment obligations before proceeding with any application.

Different lenders may offer different products and terms.

Internal Resources

Helpful information available on our website includes:

- /about-us

- /contact-us

- /privacy-policy

- /terms-and-conditions

- /advertising-disclosure

- /personal-loan-calculator

- /debt-consolidation-loans

- /bad-credit-loans

Additional Information About Personal Loans Online

Educational resources regarding Personal Loans Online can help consumers better understand application procedures, disclosure requirements, and responsible borrowing practices.

External Resources

Consumers seeking additional information may find these resources useful:

- Consumer Financial Protection Bureau

- Federal Trade Commission

- Federal Deposit Insurance Corporation

- Federal Reserve Consumer Resources

- Annual Credit Report

Additional Information About Personal Loans Credit Union

Consumers evaluating Personal Loans Credit Union offerings should review membership requirements, loan disclosures, and repayment obligations before accepting financing.

Additional Information About Personal Loans Interest Rates

Understanding Personal Loans Interest Rates is essential when comparing loan offers because interest charges may significantly affect total borrowing costs.

Final Truth in Lending Statement

At SmallPersonalLoansOnline.com, we believe transparency and education help consumers make better financial decisions. Borrowers should carefully review all disclosures, understand repayment obligations, compare multiple offers, and evaluate affordability before accepting financing.

Responsible borrowing begins with understanding the full cost of credit, including interest rates, fees, repayment terms, and total payment obligations.

Affiliate Disclosure: We are an affiliate marketing website and may receive compensation from lending partners. We are not a lender, do not make credit decisions, and do not guarantee approval. Loan terms and rates are determined by individual lenders.